Every day, individuals face unanticipated costs that can threaten financial stability. From a sudden car breakdown to an unexpected medical bill, these shocks can force us to deplete long-term savings or incur high-interest debt. Building a robust financial buffer extends beyond a simple emergency fund, offering layered protection against a wider range of scenarios.

While a traditional emergency fund typically covers three to six months of essential living expenses, a comprehensive buffer integrates additional strategies to preserve wealth and foster resilience. This article guides you through the fundamentals, personalization factors, multi-layered tactics, and evidence-based benefits of an expanded financial buffer.

Understanding the Emergency Fund Foundation

An emergency fund is nothing more than a cash reserve for non-budgeted shocks that prevents dipping into long-term investments or resorting to high-interest credit. It serves as the first line of defense against unplanned crises, such as job loss, vet bills, or urgent home repairs.

Experts recommend sizing this fund based on income stability and fixed expenses. Those with secure salaries and low living costs may aim for three months of essentials, while freelance professionals or households with high fixed obligations often target six months or more.

Place your emergency fund in a high-yield, FDIC-insured savings or money market account. Automate contributions to build steadily, and isolate these funds from everyday spending to resist temptation.

Personalizing Your Financial Buffer

No one-size-fits-all rule applies when determining buffer size and composition. Personalization matters. Assess your unique circumstances by examining essential expenses, recovery time, and exposure to risk. A self-employed consultant with fluctuating monthly income requires a larger buffer than someone in a stable occupation.

Consider dependents, health needs, and regional job market conditions when estimating potential downtime. During economic downturns, extending your buffer can mean the difference between weathering a storm and facing financial distress.

Adopt a mindset of personalization based on risk factors—not rigid formulas. Revisit your buffer annually or after major life changes, such as a new child or career shift.

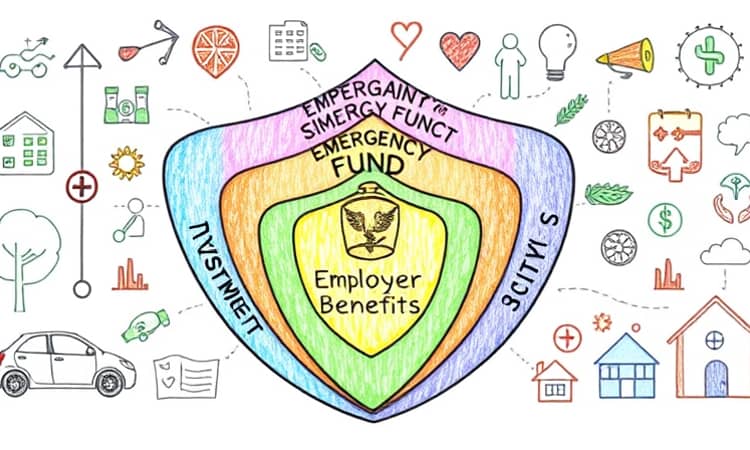

Strategies to Build a Multi-Layered Buffer

- Sinking Funds for Predictable Expenses: Create separate accounts earmarked for known irregular costs like holiday gifts, annual insurance premiums, or tech upgrades to preserve your core emergency fund.

- Investments as a Supplementary Buffer: Allocate a portion of reserves to low-risk, liquid assets like short-term bond ETFs or high-dividend stocks, acknowledging potential volatility but earning growth over idle cash.

- Employer Benefits and Matches: Maximize 401(k) or pension matching to capture "free money" and grow retirement reserves that act as a backstop when emergencies strike.

- Budget Integration: Adapt the 50/30/20 rule to funnel discretionary cuts into buffer building, ensuring that every dollar has a purpose.

- Business and Personal Separation: For entrepreneurs, maintain distinct business reserves to cover payroll and operational costs, safeguarding both ventures and personal finances.

Combining these tactics creates a layered structure that moves beyond simple cash savings, supporting both short-term security and long-term growth.

Implementing and Maintaining Your Buffer

Consistency is key. Automate transfers for consistent savings each payday, even if the amount is modest. Starting small and scaling up over time reduces stress and fosters habitual saving.

Track progress with simple spreadsheets or budgeting apps, and set milestones to celebrate improvements. If you tap into your emergency fund, prioritize replenishment before redirecting new income toward investments.

Benefits and Evidence Supporting Robust Buffers

Research shows that holding at least $2,000 in liquid savings correlates with a 21% increase in well-being and reduces financial hardships for up to three years. Households with buffers exceeding $2,500 experience fewer debt spirals and lower stress levels.

Beyond numbers, a comprehensive buffer reduces financial stress and anxiety, empowers decision-making during career transitions, and prevents forced liquidations of long-term assets.

Case Study: Gradual Buffer Building in Action

Meet Sarah, a freelancer with fluctuating monthly income. She began by setting aside $50 per paycheck into an emergency fund. After six months, she redirected the same amount into a sinking fund for anticipated car repairs and holiday expenses.

By year two, she opened a low-cost bond ETF account, allocating 5% of her monthly revenue to an investment buffer. Sarah’s layered approach ensured she never missed payments, even during lean months, and continued to grow her net worth without incurring debt.

Review and Adapt Your Buffer Over Time

- Schedule quarterly check-ins to adjust contribution levels.

- Align buffer components with evolving goals and income.

- Rebalance between cash, sinking funds, and investments based on market conditions.

Conclusion

Building a financial buffer beyond the emergency fund is an empowering journey toward resilience and growth. By embracing strategies for comprehensive financial protection and customizing your plan, you create a safety net that adapts to life’s unpredictability. Begin today, review regularly, and watch your confidence—and net worth—flourish.